Modern Monetary Theory Is Too Good To Be True

Source: Adobe/Yulia Lisitsa.

The Australian federal government is preparing to invest AUD 190 billion (USD 132 billion) to support the economy in action to COVID-19, according to the most recent Parliamentary Budget Office price quote.

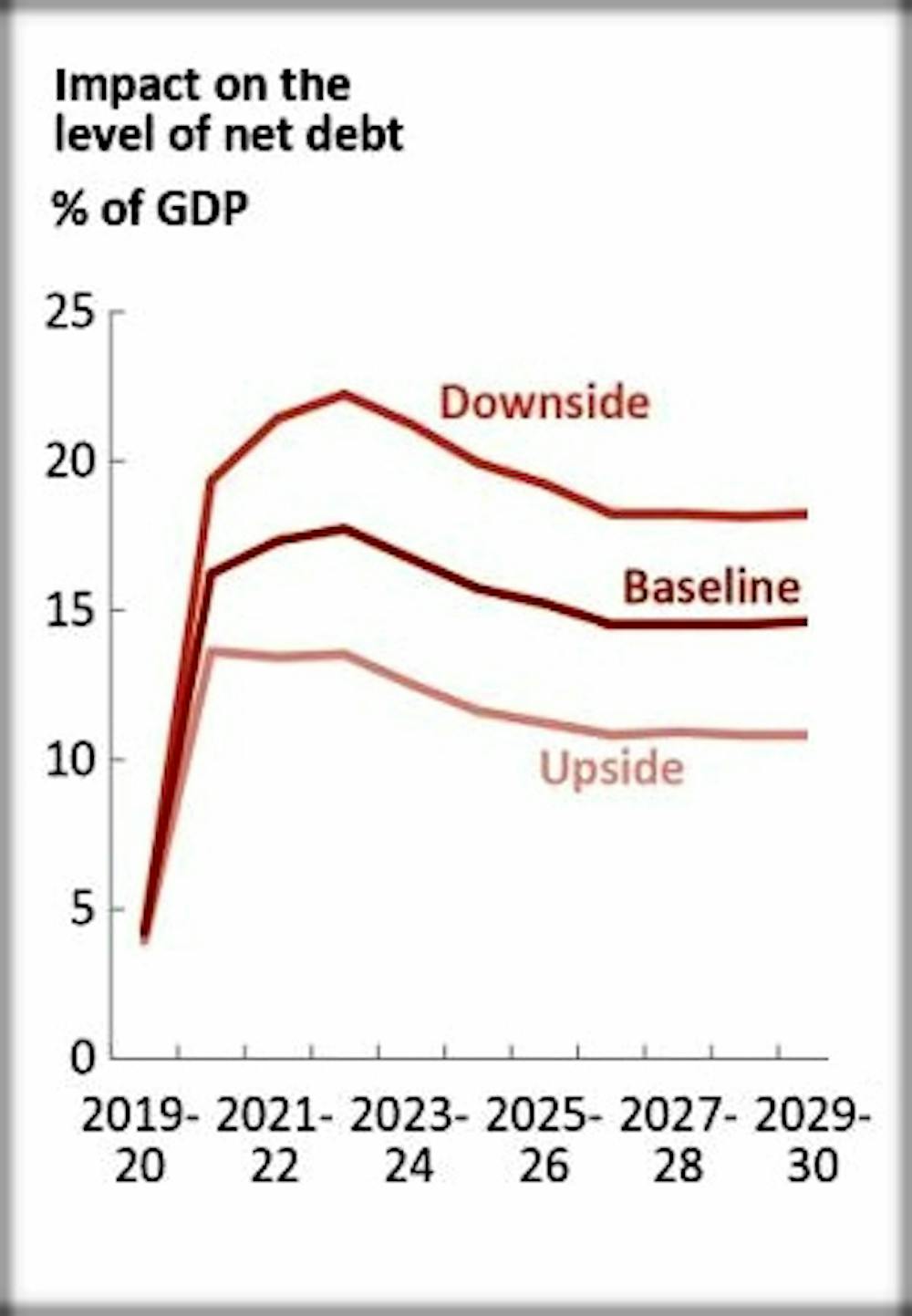

The overall effect of COVID-19 on the federal government’s net financial obligation, consisting of both earnings effects (down, since of less activity) and costs effects (up since of investing to support the economy) totals up to in between 11% and 18% of gdp, or AUD 500 billion to AUD 620 billion.

{kind=link}

The price quotes are based upon the 3 possible circumstances developed by the Reserve Bank: “downside”, “baseline” and“upside” Each vary in their presumed timing of the relaxation of social distancing and other constraints, and for how long unpredictability and reduced self-confidence weigh on families and business activity.

With comparable blow-outs all over the world, a view acquiring ascendancy, consisting of among analysts such as Alan Kohler, is that federal government financial obligation does not matter– offered the federal government owes the money to its main bank (in Australia’s case, the Reserve Bank) or the bank is prepared to purchase the financial obligation from the party the federal government obtained the money from.

The view is an application of so-called modern monetary theory and the argument goes like this:

-

when the federal government runs a budget deficit, it obtains from the private sector (primarily financial organizations) by offering federal government bonds which are successfully IOUs using to pay back in a particular variety of years and using interest at a low bond rate up until then

-

the Reserve Bank (together with other reserve banks) has actually been purchasing bonds from the private sector with money it creates, and states it is prepared to purchase as lots of as are needed to keep the bond yield low, so that if it appears the bond rate will rise, much of the financial obligation will eventually be owed to the bank

-

when the bonds end and it is time to pay back the financial obligation, the federal government can just provide more bonds which the bank will eventually purchase if it needs to in order to keep the bond rate low

-

if down the track all of the additional money in the banking system triggers inflation, the procedure would be tossed into reverse, decreasing inflation.

It sounds too good to be true, since it is.

There are a variety of reasons deficits and financial obligation do matter, even if the financial obligation is successfully owed to the main bank and even if it has actually been produced in an economic downturn, or in anticipation of one– as holds true for the COVID-19 action.

Developing money brings threats

We understand that federal governments with high financial obligation face interest rate premiums from lending institutions. A European Union study discovered that a 10 portion point boost in the federal government financial obligation to GDP ratio increased the sovereign bond rate by 0.47 portionpoints

.

These greater threat premia circulation on to private sector customers whose rates of interest are embeded in relation to sovereign rates of interest, so all companies and families deal with greater rates. The result will be less financial investment and home costs than there would otherwise be.

An effort by the main bank to negate the threat premium by purchasing more bonds would permit the federal government to provide even more bonds, increasing the threat of inflation which would itself put upward pressure on rates of interest.

Read more:.

Explainer: what is modern monetary theory?

The experience of Latin American countries that depend on their reserve banks to develop money is frightening. Argentina and Venezuela in specific knowledgeable inflation rates of approximately 50% and dropping currency exchange rate.

The concept that, if and when inflation shows up, the Australian federal government might quickly toss its costs and tax engines into reverse is fanciful. It is politically tough to wind back federal government costs and raise taxes. To do so on a big scale may be difficult.

Modern Monetary theorists react by mentioning that we have actually not yet seen inflation in Western countries that have actually pumped up their money products.

That’s true, however while the federal government has actually been adding financial obligation, we have actually seen inflation of a sort in big increases in possession costs in real estate and stock exchange.

It has actually made us more susceptible to financial shocks and priced lots of first home purchasers out of the market.

Markets aren’t flexible

Markets aren’t constantly flexible.

And what if the forex market does not purchase the modern monetary theory story?

Even the expectation of future inflation by the market, prior to it shows up, might lead to a devaluation of the Australian dollar which might itself develop inflation which would make Australians poorer.

A final point: the Reserve Bank of Australia is independent from the federal government.

If self-confidence in this self-reliance was worn down, we might see a boost in viewed threat of holding Australian financial properties. This, in turn, would trigger greater rates of interest and a lower Australian dollar.

In any case, the Reserve Bank may choose at some time that the threat of inflation or possession rate inflation is inappropriate and decline to purchase more federal government bonds, or offer back to the private sector the bonds it’s purchased.

Read more:.

Vital Signs. Do deficits matter any more?

When again,

This would imply the federal government financial obligation was owed to the private sector. Financial markets may see it as riskier than financial obligation owed to the bank, with unfavorable repercussions for rates of interest and the exchange rate.

I am inclined to concur with the International Monetary Fund’s primary economic expert who stated in relation to modern monetary theory prior to the COVID crisis that there was “no free lunch“.

Martin Wolf of the Financial Times stated throughout the crisis that modern monetary theory was bothright and wrong

.

It was right, since there is no easy budget restraint. It was incorrect, since it would show difficult to handle the economy smartly as soon as political leaders thought there was no easy budget restraint.

Ross Visitor, Teacher of Economics and National Senior Mentor Fellow, Griffith University

This post is republished from The Conversation under an Innovative Commons license. Check out the original article.

____

Learn more:

Bitcoin vs. Modern Monetary Theory

Bitcoiners Ask: ‘WTF Happened In 1971?’ The Response May Forming The 2020 s

The post Modern Monetary Theory Is Too Good To Be True appeared first on World Weekly News.